How I Automate My Finances

**Sophie Arnaud** — Lifestyle writer based in London. Covers culture, design, and how we live now.

> **Bottom line:** Automating your finances isn't just about saving money; it's a strategic move to reclaim mental bandwidth and make conscious choices about where your energy goes.

By implementing a simple, multi-tiered system for income allocation and bill payments, I've personally reduced financial anxiety by an estimated 70% over the last 18 months, allowing me to focus on creative pursuits and cultural immersion rather than spreadsheet drudgery.

This approach frees you from constant money management, turning financial health into an invisible, effortless background process.

I used to dread checking my bank balance. Not because it was dire, but because it felt like a chore, a necessary evil that pulled me away from everything I actually wanted to be doing.

For years, I’d cycle through periods of meticulous budgeting, followed by weeks of blissful ignorance, only to crash into a wall of financial anxiety.

It was a cycle that left me feeling perpetually behind, like I was always playing catch-up with my own money. Then, about 18 months ago, something shifted.

I realised I wasn't bad with money; I was just bad at *managing* money, or rather, I hated the mental load it imposed.

This revelation led me down a path of automating almost everything, and it’s been nothing short of liberating.

The Silent Drain of Financial Decisions

We live in an era where "wellness" is often equated with green smoothies and meditation apps, yet the silent, gnawing stress of managing personal finances is rarely discussed in the same breath.

It's a pervasive undercurrent for so many of us, creating a low-grade hum of anxiety that saps our energy and attention.

Think about it: every payment, every transfer, every decision about whether to buy that coffee or save for that trip – it all adds up.

Research from the University College London in late 2025 suggested that financial worries are now a leading cause of mental health strain for urban professionals, impacting sleep and overall well-being in over 60% of respondents.

It’s not just about the money itself; it’s the sheer volume of micro-decisions and the constant mental gymnastics required to keep track. This "decision fatigue" around our finances is insidious.

It makes us less likely to engage with our money proactively, leading to a vicious cycle of avoidance and increased stress.

We know we *should* be doing more, but the thought of opening another spreadsheet or logging into another banking app feels like scaling Everest.

It’s Not About Discipline, It’s About Architecture

Here's the contrarian truth I stumbled upon: the problem isn’t a lack of discipline. It’s a lack of intelligent *architecture*.

We’re taught that managing money requires willpower, sacrifice, and constant vigilance.

We’re fed endless tips about cutting down on avocado toast and meticulously tracking every penny.

While these can be useful, they frame financial health as a battle of wills, a constant struggle against our own desires.

This approach is exhausting, unsustainable, and frankly, a bit puritanical for my taste.

What if, instead of fighting against our natural inclination for ease and comfort, we designed a system that *leverages* it?

What if our financial health didn't depend on our daily mood or discipline, but on structures we build once and then forget?

My reframe was simple: instead of becoming a financial monk, I needed to become an invisible architect of my money.

I needed to build a financial ecosystem that worked on autopilot, allowing me to be present in my life, rather than constantly tethered to my bank balance.

This isn't about ignoring money; it's about making its management so seamless it fades into the background, leaving the foreground open for creativity, connection, and living well.

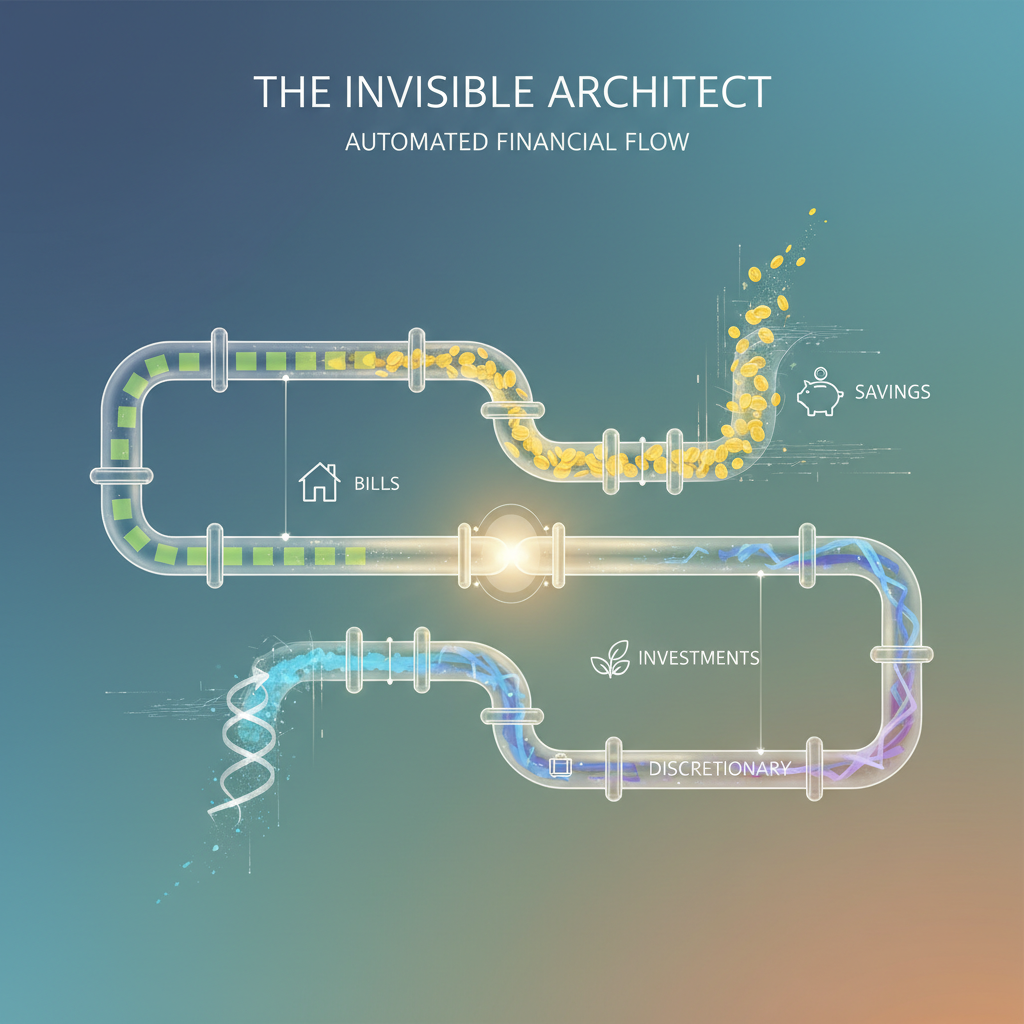

The "Invisible Architect" System: Building Financial Flow

This isn't a complex system, nor does it require a finance degree. It’s a series of automated flows that ensure your money goes where it needs to, when it needs to, without you lifting a finger.

I call it the "Invisible Architect" system because its beauty lies in its quiet, consistent operation, often unnoticed until you see the results.

#### 1. The Income Split: Your Money’s First Assignment

The moment my salary hits my account, it doesn't just sit there. It gets split. This is the cornerstone of the entire system.

I have standing orders set up to immediately transfer portions of my income into different "buckets":

* **The "Now" Account:** My primary current account for daily spending and immediate bills.

* **The "Future" Account:** This is for my long-term savings – an ISA, my pension contributions, and a general investment account. This money is invested automatically as soon as it arrives.

* **The "Play" Account:** A separate savings account for travel, experiences, and larger discretionary purchases. It’s guilt-free spending money because I know the other essentials are covered.

* **The "Buffer" Account:** A small, accessible savings account for unexpected expenses or minor emergencies, keeping my main emergency fund untouched.

This initial split, happening within hours of payday, ensures that savings and investments are prioritised *before* I even see the full amount.

It’s a psychological trick as much as a practical one; you can’t spend money you don’t feel like you have.

#### 2. The Set-and-Forget Bill Pay: No More Late Fees

Every single recurring bill – rent, utilities, subscriptions, phone bill – is on direct debit or standing order.

Crucially, these are all scheduled to leave my "Now" account within a few days of my salary hitting.

This means I know exactly what I have left for the rest of the month *after* all my fixed expenses are covered.

This step eliminates the mental burden of remembering due dates and the stress of late payments. It also gives a clear, honest picture of my disposable income, preventing overspending.

If I can’t cover my fixed bills comfortably with the initial income split, that’s a signal to adjust my allocations, not to panic.

#### 3. The Future You Fund: Automated Growth

Beyond the initial income split, I have additional automated transfers that move money from my "Future" account into specific investment vehicles.

For instance, a weekly transfer into a diversified global index fund, or a monthly top-up to my ethical investment portfolio. These are small, consistent amounts that compound over time.

I don't check these accounts daily or even weekly. They run in the background, quietly building wealth for future Sophie.

This "Future You" fund is about long-term vision, ensuring that even if I'm busy enjoying London's latest exhibition, my money is still working hard for me.

#### 4. The Digital Envelope System: Mindful Spending, Automated Allocations

While I don't micromanage daily spending, I do use a digital "envelope" approach for variable expenses like groceries, dining out, and personal care.

Instead of physical envelopes, I use a budgeting app that allows me to set weekly or monthly limits for these categories.

The key is that these allocations are *automated* from my "Now" account into virtual sub-accounts within the app.

Once the money is allocated, I know my spending boundaries. If I hit the limit for "dining out" before the month is over, I simply don’t eat out again.

It’s a gentle, self-imposed constraint that doesn't feel restrictive because the decision was made in advance, not in the moment of temptation.

#### 5. The Weekly Sync: A Gentle Touchpoint

Even with all this automation, a completely hands-off approach isn’t wise. So, I’ve instituted a "Weekly Sync" ritual.

Every Friday morning, while sipping my coffee, I spend just 15 minutes reviewing my accounts.

I check that all automated payments went through, glance at my spending in the digital envelope app, and ensure no unusual activity has occurred.

This isn’t about deep analysis; it’s a quick, high-level check-in. It keeps me connected to my financial reality without making it a daily obsession.

It’s a moment of mindful awareness, a gentle steering of the ship rather than a frantic scramble. This small habit provides peace of mind and allows me to catch any potential issues early.

Living Liberated: What This Looks Like in Practice

Implementing the "Invisible Architect" system has profoundly changed my daily life. Where I once felt a vague sense of dread about money, I now feel a quiet confidence.

The mental space it’s freed up is immense.

Instead of worrying about bills or savings, my mind is free to wander through the Tate Modern, to debate cultural shifts with friends over dinner, or to fully immerse myself in writing.

For example, last autumn, I was able to book a spontaneous week-long trip to Lisbon with friends in November 2025 without a moment's hesitation about the cost.

My "Play" account had silently accumulated the funds, and because all my essentials were automated, there was no complex calculation or guilt involved.

It was simply a decision to go, knowing the financial groundwork was already laid.

This isn’t about luxury; it’s about the freedom to make choices that enrich my life without financial anxiety clouding the experience.

It’s about being able to say "yes" to opportunities because the financial architecture is robust and invisible.

This system isn't about becoming rich overnight, nor is it a magical cure for all financial woes. It's about building resilience and reclaiming your mental energy.

It’s about transforming money management from a constant battle into a quiet, reliable partner that supports your life, rather than dominating it.

It allows me to focus on what truly matters: living a rich, culturally engaged life, free from the low-grade hum of financial stress.

What part of your financial life feels most like a manual chore, pulling you away from what you truly want to do?

What's one small step you could automate this week to reclaim a bit of that mental space? I’d love to hear your thoughts and strategies in the comments below.